What Business Owners Should Know About SBA Loan Options

PAGE

By PAGE Editor

What Are SBA Loans?

Small business owners often look for ways to get extra money to grow their companies. This could be for buying new equipment, getting more inventory, or even just covering day-to-day costs. The Small Business Administration, or SBA, offers a way to get these funds. SBA loans are not directly given by the SBA itself. Instead, the SBA works with banks and other lenders. They guarantee a portion of the loan, which makes it less risky for the lender. This guarantee means more businesses can get approved for the funding they need. It's a way for the government to support small businesses.

How SBA Loans Differ from Traditional Loans

When you compare SBA loans to regular bank loans, there are some key differences. Traditional loans often have stricter requirements and can be harder to get approved for. SBA loans, because of the government guarantee, can sometimes offer more flexible terms. This might mean longer repayment periods or lower down payments. The SBA sets guidelines, but the actual loan is processed through an SBA-approved lender. This partnership helps bridge the gap for businesses that might not qualify for traditional financing. It's a good option to consider when other avenues seem closed.

The Role of the SBA in Lending

The SBA plays a specific role in the lending process. They don't hand out cash directly, except in cases of disaster relief. Their main job is to reduce the risk for lenders. By guaranteeing a part of the loan, the SBA encourages banks to lend to small businesses. This makes it easier for entrepreneurs to access capital. The SBA also provides resources and sets standards for these loans. They want to make sure small businesses have a fair chance to get the money they need to succeed. Think of the SBA as a partner that helps make loans happen.

Key SBA Loan Programs Available

The U.S. Small Business Administration (SBA) doesn't lend money directly, except in disaster situations. Instead, it works with banks and other lenders to guarantee a portion of the loan. This reduces the lender's risk, making it easier for small businesses to get the funding they need. Understanding the different SBA loan programs is the next step after knowing what SBA loans are.

There are several main types of SBA loans, each designed for different business needs. The most common ones are the 7(a) loan program, the 504 loan program, and microloans. Each has its own set of rules and purposes, so it's important to figure out which SBA loan program fits best.

The Versatile 7(a) Loan Program

The 7(a) loan program is the SBA's flagship offering, known for its flexibility. It's suitable for a wide range of business needs, from working capital and equipment purchases to business acquisitions and refinancing existing debt. The maximum loan amount under this program is $5 million.

This program is great because it can be used for so many things. Think of it as the all-purpose SBA loan. It's designed to help businesses grow and operate smoothly. The 7(a) loan is the most common type of SBA-backed loan.

Within the 7(a) umbrella, there are also specialized options like CAPLines for short-term cash flow needs and Community Advantage loans for businesses in underserved areas. SBA Express loans offer faster processing for smaller amounts, up to $500,000.

The 504 Loan for Fixed Assets

The 504 loan program is specifically for businesses looking to finance major fixed assets. This typically includes purchasing land, buildings, or long-term machinery and equipment. The goal here is job creation and economic development.

These loans come with long-term, fixed interest rates, which can be very attractive for large investments. The SBA guarantees a portion of the loan, while a bank or credit union provides the rest, and a Certified Development Company (CDC) often handles the SBA-guaranteed portion.

Key features of the 504 loan include:

Purpose: Primarily for fixed assets like real estate and equipment.

Loan Amount: Up to $5 million, though specific limits can apply.

Terms: Typically 10 to 25 years, with fixed interest rates.

Job Creation: Often a requirement to demonstrate how the loan will create or retain jobs.

Microloans for Smaller Needs

For businesses that need smaller amounts of capital, the SBA Microloan program is a good option. These loans are for $50,000 or less and are provided through intermediary lenders, like non-profit organizations.

Microloans are often used for working capital, inventory, or supplies. They can be particularly helpful for startups or very small businesses that might not qualify for larger loan programs. The repayment terms are usually shorter, often around six years.

These smaller loans can make a big difference for businesses needing just a little boost to get over a hump or make a specific purchase. They are a vital part of the SBA's mission to support all sizes of small businesses.

Disaster Loans for Recovery

SBA disaster loans are a bit different. These are direct loans made by the SBA itself, not through partner lenders. They are specifically for businesses, homeowners, and renters affected by declared natural disasters.

The purpose of these loans is to help individuals and businesses recover and rebuild after a disaster. The terms and amounts vary depending on the extent of the damage and the specific disaster declaration. These are a critical safety net when unexpected, widespread damage occurs.

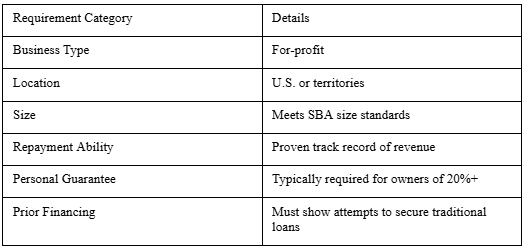

Eligibility Requirements for Business SBA Loans

General Business Eligibility Criteria

To even be considered for an SBA loan, your business needs to meet a few basic criteria. First off, it has to be a for-profit venture. Non-profits generally don't qualify for these specific loan programs. Also, your business must be operating legally within the United States or its territories. This means having all the necessary registrations and licenses in place. The SBA wants to support legitimate businesses that contribute to the U.S. economy.

Beyond that, the SBA has specific size standards that businesses must meet. These standards vary by industry, so it's important to check where your business falls. Generally, the SBA considers a business "small" if it meets these industry-specific employee or revenue thresholds. If your business is too large, you won't be eligible for SBA loan programs, even if you meet other requirements. It's a key part of the SBA loan eligibility puzzle.

Financial and Creditworthiness Standards

Lenders will look closely at your business's financial health. They need to see that your business has a solid plan and the ability to repay the loan. This usually means having a history of steady or increasing revenue. Lenders often require at least two years of operation, though some programs might have different timelines. Startups without a proven track record typically find it harder to get approved for SBA loans.

Your personal credit score also plays a significant role, especially if you own 20% or more of the business. While the SBA doesn't set a strict minimum credit score, most lenders prefer applicants with scores of 690 or higher. They'll also want to see your business and personal tax returns for the past three years. This helps them get a full picture of your financial situation and your capacity to handle new debt. Creditworthiness is a major factor.

The Need for Alternative Financing

One of the core principles behind SBA loans is that they are meant to fill a gap when traditional financing isn't readily available. This means you generally need to show that you've tried to get funding from other sources first. Banks, credit unions, and other private lenders are the first stop. If they turn you down or can't offer terms that work for your business, then an SBA loan becomes a more viable option.

This requirement is often referred to as exhausting alternative financing options. You'll likely need to provide documentation of these previous attempts. The SBA wants to make sure its guaranteed loans are going to businesses that genuinely need this type of support and can't secure it elsewhere on reasonable terms. It's not just about needing money; it's about needing it when other doors have closed. This is a critical part of SBA loan eligibility.

Businesses must demonstrate they've explored other financing avenues before applying for an SBA loan.

Benefits of Choosing Business SBA Loans

Competitive Interest Rates and Terms

SBA loans often come with interest rates that are lower than what you might find with traditional bank loans. This is because the SBA guarantees a portion of the loan, reducing the risk for the lender. This guarantee allows banks to offer more favorable terms to small businesses. These competitive rates can significantly reduce your overall borrowing costs over the life of the loan. Business owners evaluating business sba loans can compare this benefit with King Capital’s SBA financing options, which emphasize long-term funding, competitive rates, and higher borrowing limits.

Extended Repayment Periods

One of the major advantages of SBA loans is the potential for longer repayment terms. Depending on how the funds are used, you could have up to 10 years for working capital or equipment, and even up to 25 years for real estate purchases. This extended timeline can make monthly payments more manageable, freeing up cash flow for your business operations.

Flexible Use of Funds

SBA loans offer a good deal of flexibility regarding how you can use the money. Whether you need funds for starting a business, expanding operations, purchasing equipment, acquiring real estate, or managing working capital, there's likely an SBA loan program that fits your needs. This versatility makes SBA loans a strong option for various business growth stages.

Lower Collateral Requirements

While some SBA loans may require collateral, the requirements can often be less stringent compared to conventional loans. The SBA guarantee itself can sometimes offset the need for extensive collateral. Additionally, some SBA loan programs might have lower down payment requirements, making it easier for businesses to secure the necessary funding without tying up significant assets.

Navigating the SBA Loan Application Process

Working with SBA-Approved Lenders

Applying for an SBA loan means you'll be working with a bank or credit union that's been approved by the Small Business Administration. These lenders follow SBA guidelines, but they also have their own requirements. It's smart to look for a bank that actively works with SBA loans, especially a "Preferred Lender." These lenders can often make decisions faster because they don't need to send everything to the SBA for final approval. This can really speed things up.

The Importance of Lender Match

Finding the right lender can feel like a big task. That's where the SBA's Lender Match tool comes in handy. It's a free service that helps connect businesses with SBA-approved lenders in their area. You provide some basic information about your business and what you need the loan for, and the tool suggests lenders who might be a good fit. This can save you a lot of time and effort compared to cold-calling banks.

Understanding Application Timelines

SBA loan applications can take time. From submitting your paperwork to getting approved and finally receiving the funds, it's not usually an overnight process. Be prepared for a waiting period that can range from a few weeks to a couple of months. Having all your business documents organized beforehand can help speed things up. Always ask potential lenders about their typical timelines.

The Role of a Personal Guarantee

One thing to know about SBA loans is that they almost always require a personal guarantee. This means that if the business can't repay the loan, the owner is personally responsible for the debt. This is a standard part of the SBA loan process, and lenders will want to see it. It's important to understand this commitment before you apply for an SBA loan.

A personal guarantee is a serious commitment. It means your personal assets could be at risk if the business struggles to repay the loan. Make sure you're comfortable with this before moving forward.

Potential Drawbacks of Business SBA Loans

While SBA loans offer many advantages, business owners should be aware of potential downsides before applying. These loans, backed by the Small Business Administration, are designed to help small businesses, but they aren't always the quickest or simplest funding option. Understanding these drawbacks can help business owners prepare and manage expectations.

Extended Approval and Funding Times

One of the most frequently cited drawbacks of SBA loans is the time it takes to get approved and receive the funds. Because the SBA acts as a guarantor, the process involves more paperwork and review than a traditional bank loan. Lenders need to submit applications to the SBA for approval, which can add weeks or even months to the timeline. This extended process means SBA loans might not be suitable for businesses facing immediate financial emergencies or those on a very tight deadline. For instance, a business needing capital for a time-sensitive opportunity might miss out while waiting for SBA loan approval.

Personal Guarantee Requirements

Nearly all SBA loans require a personal guarantee from the business owner(s) who own 20% or more of the company. This means that if the business defaults on the loan, the owner is personally responsible for repaying the debt. This can put personal assets at risk. It's a significant commitment that business owners must be prepared for. The SBA wants to see that owners are invested in the success of their business, and a personal guarantee is a key part of that.

Collateral and Down Payment Considerations

While SBA loans can sometimes have lower collateral requirements compared to traditional loans, they are not always absent. Lenders may still require collateral to secure the loan, and the amount can vary. Additionally, some SBA loan programs, like the 7(a) loan, might require a down payment from the borrower, typically ranging from 10% to 30% of the total project cost. This upfront investment can be a hurdle for some small businesses, especially those with limited cash reserves. It's important to discuss these requirements thoroughly with your lender.

Wrapping Up Your SBA Loan Journey

So, when it comes to getting your business the capital it needs to grow, SBA loans are definitely worth a look. They aren't direct loans from the government, but rather loans from banks that the SBA backs, making them less risky for lenders. This often means better terms for you, like longer repayment periods and potentially lower interest rates compared to other options. While they do come with requirements, like a personal guarantee and sometimes collateral, the potential benefits are significant. It's a good idea to figure out exactly what you need the money for and how much you need, then explore the different SBA programs available. Using tools like Lender Match can help you find the right bank to work with, especially one that's experienced with SBA loans. Taking the time to understand these options can really make a difference for your business's future.

HOW DO YOU FEEL ABOUT FASHION?

COMMENT OR TAKE OUR PAGE READER SURVEY

Featured

Digital advertising has become increasingly complex, with businesses expecting smarter targeting, automated campaign management, and measurable performance across multiple channels.